10 Cities Where Americans Are Deepest in Debt—but Still Buy Homes!

10 Cities Where Americans Are Deepest in Debt—but Still Buy Homes!

Elnur/Shutterstock

Debt is one of those ugly/inevitable facts of life that no one likes to discuss, right up there with death, weight gain, and new seasons of “Bachelor in Paradise.” But it’s becoming impossible to ignore. With the Great Recession receding further in rearview mirrors, Americans are again hitting the gas on spending, pushing household debt levels to a record $13.5 trillion this year, according to the Federal Reserve Bank of New York. And an increasingly big chunk of that is housing debt. After all, with ever-higher home prices come ever-higher mortgages, right?

But debt burdens vary dramatically by housing market. And forget Conventional Wisdom: The places with today’s highest home prices (we’re looking at you, New York and San Fran!) are not where folks are the most debt-burdened. But make no mistake—the real estate implications of high debt loads can be huge, constraining buyers and potentially slowing price appreciation to a crawl. Correspondingly, lower debt levels can be a sign that a housing market has plenty of room to grow.

So the realtor.com® data team set out to find the places where home buyers are the deepest and the least into debt. We looked at the debt-to-income ratios—the all-important metric that accounts for all debt owed by mortgage applicants, divided by their pretax income. This ratio is a key factor in deciding how much folks will get approved for, or even if they’ll get the loan at all.

“Escalating rises in real estate prices are causing more consumers to be stretched,” says Eric Tyson, co-author of “Mortgages for Dummies,” who points out that debt-to-income ratios are rising, but have not quite hit the levels we saw during the housing bubble. “In the years ahead, we could reach the point where it really puts a lid on future price appreciation.”

To find out just how much debt home buyers have taken on, we analyzed mortgages taken out over the first eight months of 2018.* Then we calculated the median debt-to-income ratio for mortgage borrowers in the 200 largest metropolitan areas.** We limited our list to just two metros per state, to ensure some geographic diversity.

OK? So just in time for the prime Christmas buying season, let’s first check out those markets where buyers are the most stretched.

Claire Widman

1. Honolulu, HI

Median list price: $692,600

Median mortgage borrower’s debt-to-income ratio: 45.1%

voshadhi/iStock

Honolulu is dotted with high-rise condominiums with gorgeous ocean views, catering to luxury buyers from all over the world, particularly Asia. Many of these folks are so loaded they can put in all-cash offers. That pushes prices skyward, and has made it harder for locals who don’t have a few million in the bank. They’re forced to take on higher and higher debt to become homeowners.

“Everyone is competing for property here, and that’s caused prices to keep going up,” says local real estate agent Brandon Sakata, of Locations Hawaii. The limited supply of property doesn’t help matters. “When you [combine this] with the very high cost of living and jobs that don’t support this, you have home buyers stretching themselves.”

The median household income in Honolulu is only $81,300, so it’s no big surprise that many islanders are taking the biggest loans the bank will provide to get a foothold in the market. Hey, nobody ever said a ticket to paradise came cheap.

2. Riverside, CA

Median list price: $389,900

Median mortgage borrower’s debt-to-income ratio: 43.4%

realtor.com

Californians have the highest debt in the country, according to the Federal Reserve. And residents of Riverside, about an hour inland from Los Angeles, are saddled with the double whammy of lower wages along with rising home prices. A lack of inventory is continuing to push up those costs.

“I’m just shocked at the amount of payments that a lot of people are willing to accept,” says Matthew Rundle, a local mortgage banker at Westin Mortgage.

Many families are snagging single-family homes priced around $400,000 in the suburbs, with cute front yards and a view of the mountains just outside the city. As a result, monthly mortgage payments between $2,500 to $4,000 are the norm, Rundle says.

While that may sound reasonable for California, folks in Riverside aren’t exactly making bank. The median household income is just $62,000—a far cry from the $117,500 median that folks are earning up north in San Jose, CA, the center of Silicon Valley.

“Many are accepting huge payments they can’t pay off,” says Rundle.

3. Cape Coral, FL

Median list price: $299,000

Median mortgage borrower’s debt-to-income ratio: 43%

realtor.com

The streets in Cape Coral, about two hours south of Tampa, are lined with palm trees and modern, one-story homes with access to the city’s 400-mile canal system. (Venice itself only has around 30 miles.) These canals are a big draw for baby boomers seeking second homes for retirement before they’ve paid off their first abodes. Typically, they rent out their Cape Coral homes until they’re ready to retire.

But two mortgages add up to a lot of debt.

“Now you got two residences on your credit,” says local real estate broker Mike Lombardo of Old Glory Realty.

After the housing bust, buyers held off for a while. So did landlords who got burned after tenants couldn’t pay their rent anymore. But with the economy and housing market roaring back, boomers are entering the market again, says Lombardo.

Lombardo is also seeing more younger buyers buying homes—and they tend to have the highest debt-to-income ratios.

4. Lakeland, FL

Median list price: $225,000

Median mortgage borrower’s debt-to-income ratio: 43%

realtor.com

Like Cape Coral, Lakeland is another retirement community boasting plenty of 55-plus developments. But it’s also popular with younger buyers, particularly those who have been priced out of nearby Tampa, FL, where median home prices are $264,950, and Orlando, FL, at $303,200.

The problem is that many of those millennials have tons of student debt and low credit scores to boot. For example, nearly half of those who graduated Southeastern University, a Lakeland school with about 4,000 undergrads, haven’t even started to pay off their loan, three years after leaving the university.

But with housing prices on the lower side, debt isn’t preventing many buyers from becoming homeowners. The brick ranch homes that are common here sell for around $175,000. And things like flood insurance and property taxes are relatively cheap in Lakeland compared to many other Florida cities.

5. El Paso, TX

Median list price: $174,000

Median mortgage borrower’s debt-to-income ratio: 43%

DenisTangneyJr/iStock

El Paso residents are already bogged down with auto debt. Millennials in the small city that straddles the border of Texas and New Mexico have the third-highest median car loan balances in the nation, according to the online loan marketplace LendingTree. Add in mortgage debt, and locals are swimming in red ink.

“Public transportation here isn’t prevalent,” says Tom Fullerton, an economics professor at the University of Texas at El Paso. That means folks need a car to get around.

In addition, “even though housing prices are not very expensive in El Paso, the incomes are fairly low as well,” he adds. The median household income is just $44,400, well below the national median of $61,400. Smaller paychecks make it that much harder to pay off a mortgage on a modest four-bedroom home in the suburbs, going for just under $200,000.

The rest of the top 10 metros where home buyers are taking on the most debt include Stockton, CA; McAllen, TX; Greeley, CO; Las Vegas; and New York.

Now let’s take a look at where the grass is a little greener, and folks are taking on the smallest debt loads.

Claire Widman

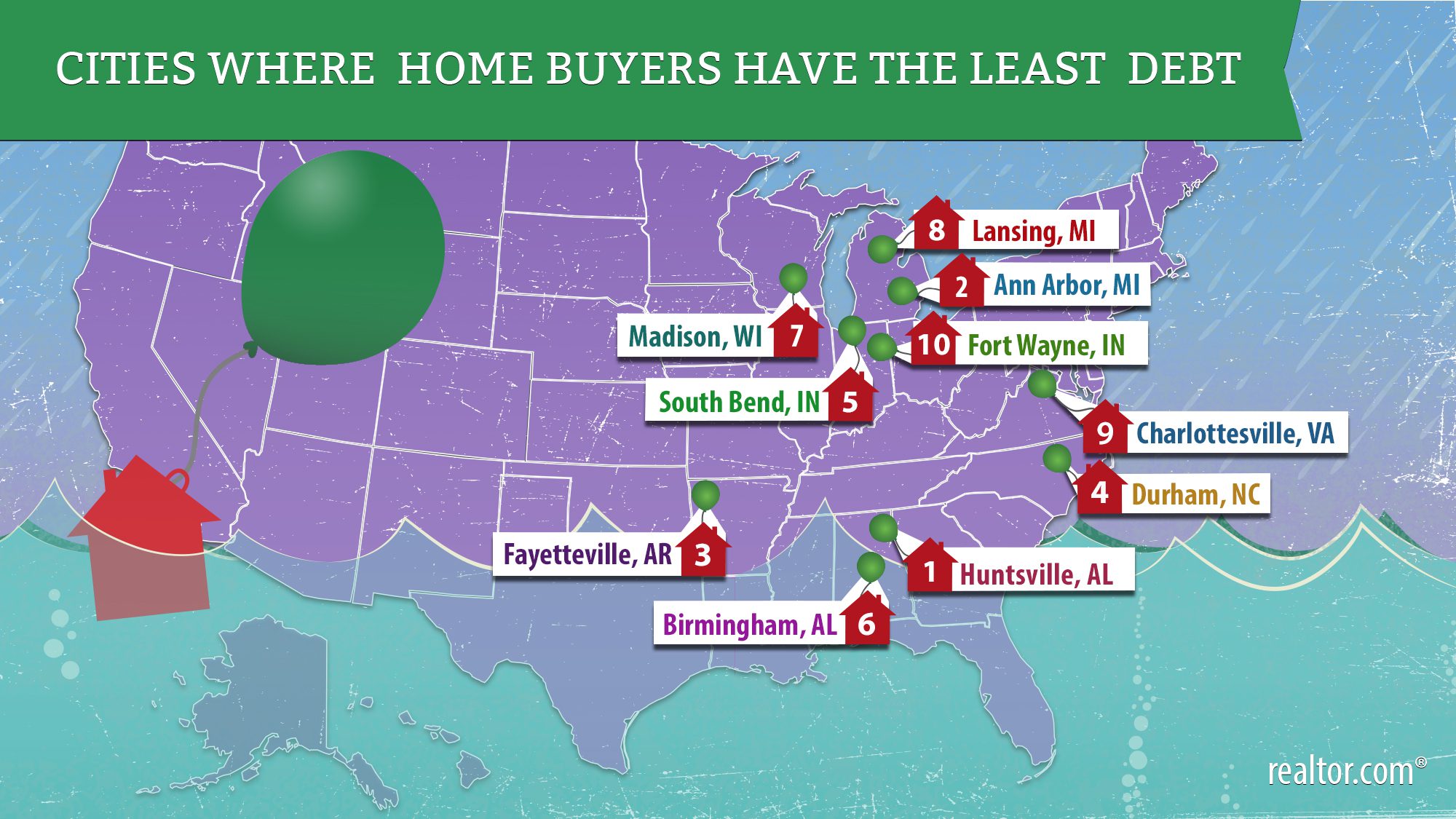

1. Huntsville, AL

Median list price: $259,100

Median mortgage borrower’s debt-to-income ratio: 33.6%

realtor.com

When you think rocket science, Alabama isn’t the first place that comes to mind. But for decades now, this town has been an aerospace hub, housing a NASA flight center and earning the nickname Rocket City. And Huntsville is still thriving, with such employers as the aircraft maker Boeing and the industrial manufacturer Siemens. This means that residents with well-paid jobs don’t need to go too much into debt to afford one of the area’s reasonably priced homes.

“Young professionals absolutely can afford to buy a home,” says Valerie Miles, a broker with Re/Max Unlimited. She also sees plenty of military families purchasing single-family homes in the region. “We have much more homeownership than renting.”

While their peers in Silicon Valley often pay seven figures for real estate, well-paid engineers in Huntsville have their choice of homes. A short drive out of downtown, home buyers will find sprawling subdivisions in communities like Big Cove, where well-appointed four-bedroom homes go for around $260,000. Now that explains why folks here aren’t exactly worried about bill collectors.

And Huntsville’s economy continues to boom. Earlier this year, Mazda and Toyota announced they would build a $1.6 billion joint plant and employ around 4,000 workers. Cue the moving vans!

2. Ann Arbor, MI

Median list price: $356,500

Median mortgage borrower’s debt-to-income ratio: 33.7%

realtor.com

Ann Arbor is another under-the-radar city that’s booming. Google recently opened a new, 130,000-square-foot, tech worker campus here (complete with on-staff barista and a massage studio, natch). Ann Arbor has grown into something of a small tech hub, where well-paid techies can take advantage of lower-cost Midwestern real estate and stay out of debt.

“We see a lot of people who are selling a home in San Francisco or Los Angeles and moving here,” says local real estate professional Deb Odom Stern of the Charles Reinhart Company. “If you’re moving from a more expensive market, you’re going to be amazed at what your money can get you.”

You’re also likely to take on less debt.

And while the typical college graduate in the class of 2017 owes around $39,000, the typical University of Michigan alumni owes just $19,000, according to U.S. Department of Education data.

This walkable college town, with its shops and pizza joints, has a number of modern condo buildings with gyms and pools that sell at around $500,000. But those trying to save some money can head to the ’burbs, where there are townhomes priced at around $275,000—within walking distance of a Whole Foods.

3. Fayetteville, AR

Median list price: $275,700

Median mortgage borrower’s debt-to-income ratio: 34.2%

DenisTangneyJr/iStock

For the sixth straight year in a row, Walmart has ranked No. 1 on the Fortune 500 list, pulling in a revenue of $500 billion for the past year. And its headquarters in Bentonville, AR, give the surrounding Fayetteville metro area quite a boost. Having Walmart here, along with Tyson Foods and J.B. Hunt, a multi-billion-dollar trucking company, means the region pulls in well-paid tech, marketing, and finance pros from all over the United States.

“Fayetteville has grown from a college town into a destination,” says local real estate agent Jill Bell of Crye-Leike.

And while folks are saving up for the standard $250,000 priced single-family home in the suburbs, they won’t be spending a ton on rent. The median rent for a one-bedroom apartment here is just $593, according to the U.S. Department of Housing and Urban Development.

4. Durham, NC

Median list price: $360,000

Median mortgage borrower’s debt-to-income ratio: 34.5%

realtor.com

Durham continues to flex its tech and engineering muscles, as the region attracts more skilled workers. In fact, Apple appears close to opening up a new campus in Durham’s Research Triangle Park. The campus is home to around 170 companies offering countless tech, data, and engineering jobs.

And unlike in many tech hubs, builders in Durham are answering the need for more homes. New construction makes up around 35% of houses listed on realtor.com in Durham. Streets in communities like Sherron Farms, a designed community, are filled with new three and four-bedroom two-story homes that come with crown molding and granite countertops. The best part? They start at around $300,000. Take that, Silicon Valley!

5. South Bend, IN

Median list price: $160,000

Median mortgage borrower’s debt-to-income ratio: 34.5%

realtor.com

News flash: South Bend isn’t Chicago. It doesn’t have the high prices (the median is $289,950 in Chicago,) expensive property taxes, and traffic of its gigantic neighbor two hours to the east on Lake Michigan. And that’s made the college town of South Bend something of a go-to for Illinois expats.

“They see how much they can get with their money,” says Beau Dunfee, managing broker at Weichert Realtors, Jim Dunfee & Associates in South Bend. “So they make the move.”

The city revolves around the University of Notre Dame and its Fighting Irish football team. The college and its respected law and business schools ensure that this city has a number of well-paid professionals. And these folks are buying up colorful 100-year-old Victorian homes that line the historic downtown.

“We really don’t see a lot of debt, because the homes are so affordable. People can easily save up for a 20% threshold,” Dunfee says. And bigger down payments mean smaller mortgages.

The rest of the top 10 metros where home buyers are in the least debt include Birmingham, AL; Madison, WI; Lansing, MI; Charlottesville, VA; and Fort Wayne, IN.

* Mortgage data is from Optimal Blue, a digital mortgage trading platform.

** A metropolitan statistical area is a designation that includes the urban core of a city and the surrounding smaller towns and cities.

Allison Underhill contributed to this story.

The post 10 Cities Where Americans Are Deepest in Debt—but Still Buy Homes! appeared first on Real Estate News & Insights | realtor.com®.

Source: Real Estate News and Advice – realtor.com » Real Estate News